The topic of how to fix your credit is becoming one that real estate professionals hear quite often these days, as the slew of short sales and foreclosures continue to work their way through the Tallahassee real estate market.

The credit repair process is so important to the recovery of the housing market that we have conducted a one-year case study to evaluate the viability of credit repair companies.

Today’s update certainly provides evidence that there is more than smoke and mirrors involved in the credit repair process.

Case Study Shows How To Fix Your Credit

First of all, if you have not read any of the previous articles in this credit repair case study, I have included the following links to catch you up to speed.

- Does Credit Repair For Homebuyers Really Exist?

- Credit Repair Update – Our Case Study Continues

- Do Credit Repair Companies Reduce The Time It Takes To Buy A Home?

- You Have A Right To Know Your Credit Score

- How To Quickly Improve Credit Score Results

- How To Repair Credit Issues That Are Stopping You From Buying A Home

These articles all point to a recurring theme … there is a process that you can follow, whether on your own or through a credit repair company.

The Right Company Knows How To Fix Your Credit

The problem with the credit repair process is that so many companies claim they can help you, but we have all heard our fair share of stories how people have been trick and mistreated, only to find that the credit repair company was nothing but a sham.

The problem with the credit repair process is that so many companies claim they can help you, but we have all heard our fair share of stories how people have been trick and mistreated, only to find that the credit repair company was nothing but a sham.

Because of this, we asked around for a credit repair company with a proven track record in order to conduct our case study. We were lead to USCCRA and Jim Hogle, and our customer “John Smith” is thrilled with their service, and here is why:

Here is an image of John’s credit report on April 1, 2013:

As you can see, his scores range from 565 to 568, thus resulting in a middle credit score of 568. This is not good and John did not qualify for any type of mortgage loan back in April.

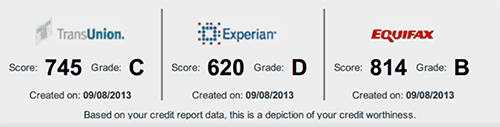

But now that we are in September, I asked John to pull a new credit report. Here is how John’s credit looks today:

So in just five months and seven days, John saw his credit score improve from 568 to 745. I would call this a success, wouldn’t you? A middle score of 745 puts John in the range to qualify for every loan product offered by most mortgage lenders.

So in just five months and seven days, John saw his credit score improve from 568 to 745. I would call this a success, wouldn’t you? A middle score of 745 puts John in the range to qualify for every loan product offered by most mortgage lenders.

Needless to say, we have been following John’s progress several times per month, and I am very impressed with the work that has been done on his behalf. Because of this, we encourage all of our credit challenged buyers to at least speak with USCCRA and see if they think they can help you.

Remember, if you have been through a short sale, foreclosure, or even bankruptcy, YOU ARE NOT ALONE!

Millions of people in the US are in the same situation, and if you do not proactively work to fix your credit, you are going to miss the boat during the real estate market recovery. Take the time to talk to Jim Hogle, and learn how to fix your credit today, you’ll be glad you did.