This scene gets played over and over in the Tallahassee real estate market.

This scene gets played over and over in the Tallahassee real estate market.

You’re in the market for a home and you find the perfect house with our property search tool, and it is priced well below market.

You think “surely this house has to be under contract already,” but when you talk to your real estate buyer’s agent, you find out that it is still available. In fact, it is a short sale, and you’ve heard about all the great short sale deals.

You quickly go look at the house, confirm that it is indeed a bargain at it’s asking price, so you make a full priced offer so as to not lose the home.

Low and behold, the seller accepts your offer, and all you need is the final step and you get the best deal of your life!

Guess what happens next?

How Short Sales Are Still Fooling Buyers

What happens next is that the contract is sent to the bank, and the bank only approves the deal if the price is within range of it’s opinion of value.

So if the house was priced well below the amount for which the bank thinks it can sell, they will not approve the sale.

They end up coming up with an “acceptable” price for which they will approve a deal, and the homeowner then sends you a counter to what was already agreed.

You have become yet another buyer fooled by the asking price of a short sale.

Think about this … Home sellers who are trying to sell “short” will get nothing at closing. Whether they sell their home for appraisal, or they sell it at a deep discount, they get nothing. So the prudent short seller prices the home low enough to get a negotiation started with the bank, and to do that, they need a contract with a buyer.

Most short sales fail to sell during their first listing period, as most “first” buyers end up cancelling the transaction when they discover they can’t have the home for the price which lured them to the home. But that first contract has let the seller know what the bank is willing to do.

When the short sale is then listed again, there is a much more “normal” asking price on the home.

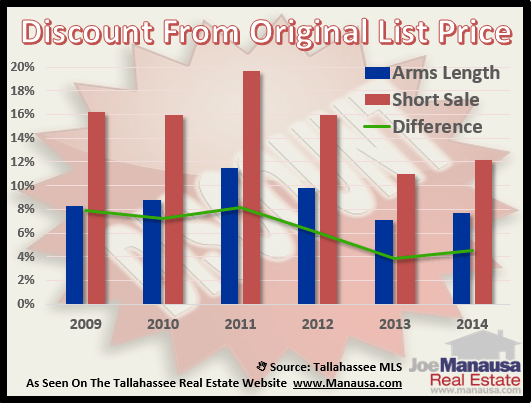

Average Discount Between Sales Price And Original List Price

The following graph attempts to measure the “discount” between sales price and list price of all homes sold in Tallahassee since the beginning of the short sale wave in 2009.

The red bars measure the difference between sales price and original list price of short sales (the discount), while the blue bars measure the discount for arms length sales.

The green lines show the difference between the two discounts.

Currently, it appears that short sales are discounted just over 4% more than are arms length sales.

It is important to note that the discount merely measures the difference between the original asking price and the final sales price, and the “original” price is merely the first price asked for the current listing period. So once a short sale is put on the market (for the second time), it is done so at a much more realistic price.

So if you are seeing a short sale listed for sale at a price that seems too good to be true, then it most likely is (too good to be true).

Guidance On Buying A Home

The moral of the story is simply “don’t be fooled by a short sale asking price.”

If you like the home, make an offer at an amount the bank is likely to accept, regardless of the asking price. If it is in its first listing period, you likely will need to offer an amount higher than its asking price, or the bank will not approve the sale.

Right now, if you buy a short sale, it appears as if you’ll get it for a little less than you would an arms length listing, but the bank is not going to be careless.

This is why we recommend you work with a well-trained real estate buyer’s agent. Take the time to learn current market conditions so that between you and your agent, you have a great understanding of real home values.