Can an AI predict one of the most complex financial shifts in modern history?

I asked ChatGPT whether the housing market would crash before 2030, and its response in the video and narrative below challenged conventional wisdom in the real estate industry. The chances of a severe downturn are higher than some expect; some experts estimate that it will occur in about one in three cases over the next five years. That’s not just a statistic; it’s a real risk that could affect anyone involved in buying or selling a home.

With millions of dollars on the line, understanding these predictions could reshape how you approach your next home purchase. So, how capable is AI when it comes to forecasting something as unpredictable as the housing market? Let’s find out!

Can AI Really Predict a Housing Market Crash?

AI’s potential to forecast a housing market crash has become a hot topic, particularly as traditional models struggle to keep pace with the market’s complexity. The housing market is shaped by a network of interconnected factors: local job growth, shifts in consumer sentiment, and global economic events all play a part. For example, changes in employment rates in your city can ripple out when combined with interest rate hikes overseas. This layered complexity is precisely why most predictions, even from seasoned professionals, fall short. And while we often hear about dramatic downturns, it’s worth noting that economic forecasters still expect positive GDP growth, not a financial crash, over the next few years.

Human behavior is the true wild card. In the same market, a modest rate dip can spur one buyer to pounce while another freezes, spooked by uncertainty. Multiply those reactions across millions of households, and predictability unravels. No wonder experts often miss the mark—history is littered with forecasts that overlooked recessions or understated rebounds. In the past 100 years, housing has crashed only three times—during the Great Depression, World War II, and the Great Recession—and each plunge has mirrored a broader economic slump. To call the next housing collapse, you’d first have to spot the next major economic downturn.

So, what sets AI—specifically ChatGPT—apart in this environment? The real advantage is in the way AI handles data. ChatGPT can process historical housing trends, economic indicators such as GDP and inflation, interest rate changes, and even real-time market shifts simultaneously. Imagine a massive jigsaw puzzle with thousands of pieces. While most economists focus on fitting together one small section, ChatGPT takes in the entire puzzle, identifying patterns and relationships that would take humans years to uncover, if they were even noticed at all. This breadth and speed enable AI to identify subtle correlations that might otherwise be overlooked as noise.

But even with this technology, no prediction is foolproof. Economic history shows that unexpected crises can blindside both human and AI models—think of the 2008 crash, which few saw coming. Still, the ability of AI to cut through the noise and highlight underlying trends is where it stands out. By parsing enormous datasets, ChatGPT can provide a clearer picture of where the market might be headed, even if it can’t guarantee certainty. And with high-profile institutions like Goldman Sachs estimating a 65% chance of recession within the next year, the need for a broad, data-driven perspective is more urgent than ever.

AI’s unique strength lies in its capacity to synthesize vast information streams and surface insights that challenge conventional wisdom. For the housing market, this means uncovering signals that could either confirm fears of a downturn or reveal hidden strengths. To see how those odds translate to home prices, keep watching.

Now, let’s look at the numbers: Why do some experts warn that a crash is inevitable, while others insist the housing market is moving through a correction?

Get Our Free Market Update

Other buyers, sellers, lenders, and real estate agents have this critical information, and now you can too!

Get immediate access to our most recent newsletter.

Let more than 30 years of experience work for you with charts, graphs, and analysis of the Tallahassee housing market.

Each Monday morning we send out a simple, one-page report that provides a snapshot of the Tallahassee housing market. It only takes 2 minutes to read, but it gives you better market intelligence than most real estate agents possess. Just tell us where to send it below!

What the Data Says About the Housing Market’s Future

Economic data paints a nuanced picture of where the housing market could be headed in the next few years. As of mid-2025, the U.S. unemployment rate stands at 4.0%, and labor force participation continues to climb with more older and prime-age workers rejoining the workforce. This resilience in the labor market has helped keep mortgage delinquencies near multi-decade lows, according to the Federal Reserve’s latest Financial Stability Report. With real disposable income keeping pace with inflation, many households are in a stronger position than they were a decade ago.

However, beneath these signs of stability, there are growing pressures. The Federal Reserve’s rate hikes since 2022 have pushed mortgage rates higher, making homeownership less affordable and discouraging homeowners with low-rate mortgages from selling. This has kept inventory tight and sidelined many would-be buyers. At the same time, financial stress is mounting in the business sector. U.S. corporate bankruptcies hit a 14-year high in 2024, and filings have already climbed another 11% year-to-date in 2025. These signals suggest that while households may be weathering the storm for now, parts of the broader economy are showing signs of strain.

Think of the housing market as a delicate seesaw. On one side, stabilizing forces—like strong bank reserves, a robust labor market, and steady consumer spending—help keep things balanced. On the other, mounting public debt, higher interest rates, and global economic uncertainty weigh things down. The balance can shift quickly if one side suddenly becomes heavier, whether due to a spike in unemployment, a global shock, or a decline in consumer confidence.

Global risks are a big part of that equation. China, for example, is experiencing GDP growth of around 4%—a far cry from its double-digit expansion in previous decades. This slowdown, tied in part to its struggling property sector, could ripple through the global economy and dampen U.S. export growth. Meanwhile, persistent trade tensions and tariff hikes have already reduced global growth by 0.3 to 0.5 percentage points, and the Caldara-Iacoviello index—used to track geopolitical risk—remains elevated. Any escalation in these risks could indirectly weigh on U.S. housing demand.

There are also warning signs in the financial markets. The yield curve, specifically the spread between 10-year and 3-month Treasury yields, has been inverted since late 2023. Historically, this has often preceded recessions. Goldman Sachs currently estimates the probability of a U.S. recession within the next year at 65%. Even so, the financial system is better prepared than it was before the 2008 crash. Banks are better capitalized, recent stress tests show that they could handle significant shocks, and the U.S. now benefits from being a net energy exporter, which reduces its vulnerability to sudden oil price jumps.

What stands out is how these data points interact. ChatGPT highlights that the interplay between historical patterns and current trends can reveal subtle vulnerabilities. Many of the variables at play—rising debt, persistent inflation, global slowdowns—mirror those seen before previous downturns. While the market appears sturdy on the surface, the underlying structure may be more fragile than it looks.

With all these pieces in play, the question isn’t just whether a crash is coming, but what kind of future the housing market is actually facing. That’s where ChatGPT’s analysis offers a new perspective.

In this video, we dive into Redfin’s April 2025 housing market update to uncover the latest trends in home prices, inventory, mortgage rates, and buyer...

I've analyzed the latest Zillow housing market report to show you the critical shifts happening in real estate markets nationwide

ChatGPT’s Prediction: The Housing Market by 2030

ChatGPT’s prediction for the housing market by 2030 is based on a detailed analysis of historical crisis frequencies, yield curve signals, and the latest economic data. When weighing the probabilities, the AI model considers a soft landing the most likely outcome, assigning it a 55% chance. This projection is based on reviewing how past downturns unfolded, comparing current yield-curve inversions, and assessing recent labor and inflation data. In this scenario, we’d see real GDP growth hover between 1% and 2%, unemployment stay at or below 5%, and inflation settle near 2%. For the housing market, this means home prices would likely stabilize, neither surging nor crashing, leading to a period of relative stability where buyers and sellers face fewer surprises. If you’re concerned about rising rates, remember that refinancing could become an option again if the rate environment shifts.

But the story doesn’t end there. ChatGPT assigns a 30% probability to a moderate recession by 2030. This scenario is based on the model’s review of economic cycles and the likelihood of two consecutive quarters of GDP decline—specifically, a drop of approximately 2%. Unemployment could rise to 6% or 7%, and national home prices may fall by 5% to 10%. Still, history suggests this drop would be temporary, with prices rebounding as the economy recovers. Even in this downturn, many homeowners could refinance if rates return to lower levels, providing some flexibility despite short-term volatility.

There’s also a smaller, but real, risk of a much sharper downturn—a full-blown crisis, which ChatGPT estimates as a 15% probability. This figure is rooted in the historical average, which is approximately three major housing crashes in the last hundred years, or roughly 3% per year. In this outcome, GDP would decline by more than 4%, unemployment would rise above 8%, and a credit crunch could hit the market. Home prices might see a drop of 15% or more. However, even in this worst-case scenario, ChatGPT points out that today’s financial system is better capitalized and regulated than it was in 2008, making a total collapse less likely. For homeowners facing this kind of uncertainty, refinancing could still be a tool to manage higher costs or lock in better terms if the market stabilizes later.

It’s important to note that these probabilities are not just pulled from thin air. ChatGPT incorporates the Federal Reserve’s June 2025 median forecast, which projects unemployment rising to 4.6%. Even small changes in the job market can shift the odds between these scenarios, as unemployment is a key signal for shifts in consumer spending and mortgage performance. The interplay of these factors is why the model emphasizes that while a crash is possible, it’s not the likely case.

However, remember that these are national odds—your local market may tell a different story. Regional factors, such as local job growth, inventory levels, and migration trends, can significantly deviate from the national average. ChatGPT’s insights are best used as a starting point, not a guarantee, for your unique plans and strategies.

If you’re hoping for a dramatic drop in home prices, the data suggests waiting for a crash may not pay off unless there’s an unexpected crisis. For most people, the market is more likely to enter a stable phase, with opportunities and risks that will depend on your timeline and local conditions.

In the aftermath of the landmark Burnett v. NAR case, the verdict has sparked a national conversation and a series of legal challenges that question...

Robo offers in real estate are transforming the traditional home selling process, bringing both opportunities and challenges for sellers.

What To Do Next

If you plan for a normal or long-term tenure, buying now often beats waiting—even if rates fall later, you can refinance, but history shows prices rarely drop enough to make waiting pay off.

<GRAPH 7>

ChatGPT’s forecast assigns a 55% chance to a soft landing, a 30% chance to a moderate recession, and a 15% chance to a sharper downturn, reinforcing that a dramatic crash is unlikely. I think a great takeaway from this video is that even the most intelligent machine in the world cannot predict the future; it can only assign probabilities based on its access to most of the data available.

Real estate decisions should be grounded in local realities. Compare your region’s job growth, inventory levels, and recent price trends against these national probabilities. Use the AI-driven insights as a framework, but let your final call be shaped by careful local research.

If you want to delve deeper into whether a housing crash is imminent, I’ve just released a new video highlighting five key points that underscore the likelihood of a crash within the next 12 months. You can view it by clicking the video below.

YOU CAN SELL A HOUSE ON YOUR OWN!

One thing you need to understand right up front is that the only differences between you and a real estate professional or another “For Sale By Owner” are knowledge and experience. Experience is tough to gain but knowledge is available right here.

Simply scan the QR code at the right (or visit www.theFSBObook.com) to secure a copy of the ultimate homeowners user manual for selling a home without paying a listing agent. Don't make the mistakes listed in the book, or you might find yourself among the 96% of FSBO sellers who fail to sell a home to somebody they didn't already know.

If you're selling FSBO, it's likely to save money, right? Follow my guide and the extra money will be there for the taking!

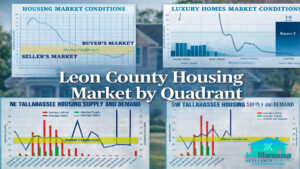

Understanding the Leon County housing market requires more than simply looking at price trends. Supply, demand, and transaction activity often vary significantly across different areas

The Tallahassee real estate market update for March 2026 shows a market that is no longer accelerating, but also not deteriorating. Tallahassee home prices appear

One thing you need to understand right up front is that the only differences between you and a real estate professional or another “For Sale By Owner” are knowledge and experience. Experience is tough to gain but knowledge is available right here.

One thing you need to understand right up front is that the only differences between you and a real estate professional or another “For Sale By Owner” are knowledge and experience. Experience is tough to gain but knowledge is available right here.